Debt Avalanche vs. Debt Snowball: Which is Best For Eliminating Debt?

After you’ve created a budget to cover your monthly expenses and have saved $1,000 in your starter emergency fund, it’s time to develop a plan to eliminate your debt for good!! Without a debt repayment plan, this can be an overwhelming and confusing task. Implementing a proven strategy will make your journey to debt freedom quicker than if you just started throwing money in multiple directions.

There are two methods that financial experts recommend for destroying your non-mortgage debt: the Debt Avalanche Method and the Debt Snowball Method. This post explains the difference between the two strategies so that you can decide which one is right for you. I’ll also tell you about the FREE debt payoff calculator I used to develop a plan for paying off my six-figure student loan debt!

Some of the links in this post are affiliate links. We may receive compensation when you click on links to products at no extra charge to you. View our full disclaimer.

Debt Avalanche vs Debt Snowball

Debt Avalanche Method

With the Debt Avalanche Method, debts are paid off in order of highest interest rate.

First, order your debts from the highest interest rate to lowest interest rate. If possible, pay more than the minimum payment on your debt with the highest interest rate. Pay the minimum amount on everything else. Once the account with the highest interest is paid off, move to the debt with the second-highest interest rate. Add your previous debt payment + any extra money to increase the amount paid on the next debt, and so on.

For example:

Department Store Credit Card = $1,200; 23% interest rate; $55 minimum

Car Loan = $7,000; 9% interest rate; $190 minimum

Student Loan = $20,000; 6% interest rate; $240 minimum

Travel Rewards Credit Card = $400; 18% interest rate; $30 minimum

Focus on your highest interest debts. With the Debt Avalanche, you would pay off the Department Store Credit Card first. Once that is paid off, you will apply its minimum payment to the Travel Rewards Credit Card each month ($55 + $30 = $85/month). Next, you’ll pay off the Car Loan ($55 + $30 + $190 = $275/month). Lastly, you’ll tackle the Student Loan. By that time, you’ll have at least $515 to pay on it each month (an extra $275)!!

Debt Snowball Method

With the Debt Snowball Method, debts are paid off in order of lowest balance.

Order your debts from lowest balance to highest balance, disregarding minimum payment amounts and interest rates. Pay the minimum amount on all debts. Pay as much as you can, in addition to the minimum payment, on the debt with the lowest balance. The extra money you plan to apply to debt each month is called your “debt snowball.” Once it is paid off, apply that minimum payment + your debt snowball to your next lowest balance. Your debt snowball will grow larger and larger as you continue adding the previous minimum payment to the next debt.

For this example, let’s say you have $100 extra to pay on debt every month:

Department Store Credit Card = $1,200; 23% interest rate; $55 minimum

Car Loan = $7,000; 9% interest rate; $190 minimum

Student Loan = $20,000; 6% interest rate; $240 minimum

Travel Rewards Credit Card = $400; 18% interest rate; $30 minimum

Debt Snowball: $100

After ordering these debts from the lowest balance to the highest balance, you will focus on paying off the smallest debts first. Start with the Travel Rewards Credit Card and apply your $100 snowball each month until the balance is $0. Once that is paid off, you will move to the Department Store Credit Card. Your debt snowball at this time will be $130 ($100 initial snowball + $30 Travel Rewards Credit Card minimum payment). Each month, you will pay $185 on the Department Store Credit Card ($130 snowball + $55 minimum payment). Once that is paid you, you’ll target the Car Loan ($185 snowball + $190 minimum payment). Lastly, you’ll tackle the Student Loan ($375 snowball + $240 minimum payment). In this example, you would be paying $615 towards your Student Loan each month, an extra $375!!

Which is Better?

Depending on your situation, one method may be better than the other. Dave Ramsey touts the Debt Snowball Method in his Total Money Makeover; however, financial experts endorse both of these methods. Neither option is a definite “winner.”

The Debt Avalanche method will help you pay off your debt faster and may also save you money on interest. The greatest challenge with this method is that it often takes a long time to pay off each debt; which means you’ll have to be persistent, even when you don’t feel motivated. However, by the time you get to the lowest interest rate, your avalanche will have picked up some serious speed.

The Debt Snowball method is excellent if you need quick wins to stay motivated along your debt freedom journey. The snowball gains momentum as you pay off smaller debts at the beginning. By the time you get to larger debts, you’ll be throwing a huge amount of money at it each month. However, you may end up paying more interest over time.

The Hybrid Approach includes a mix of both methods. If you have credit card debt (or high-interest personal loans), I recommend starting with the Debt Avalanche method, as the high-interest rates will end up costing you a lot more money over time. Once your credit card balance is $0, use the Debt Snowball method to repay your other credit accounts.

Note that paying extra on your debt each month (as we did in the second example) will help you pay them off even faster, no matter the method you’re using!

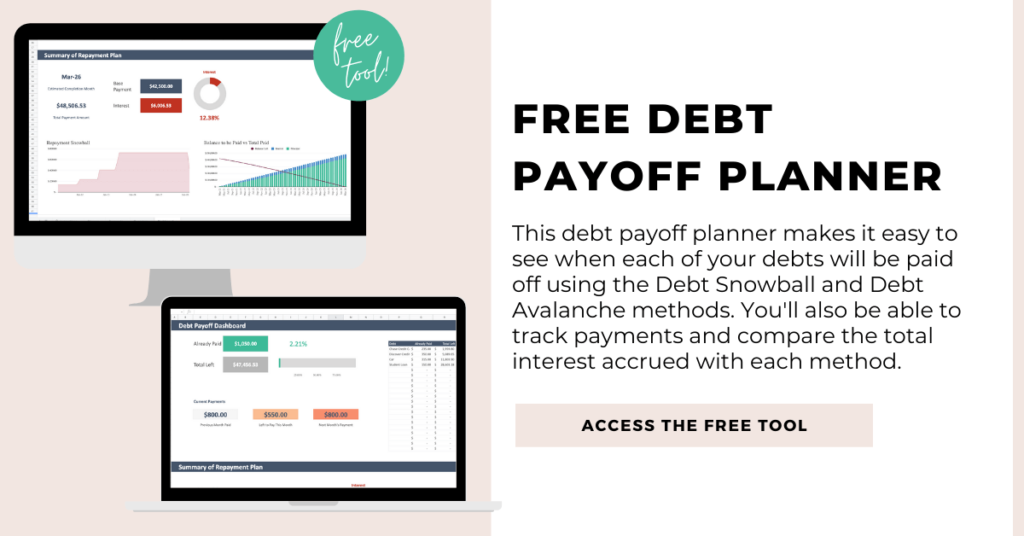

Free Debt Avalanche / Debt Snowball Calculator

I’m so glad I discovered Undebt.it, a free debt payoff calculator that will help you determine which method is best for your situation. It is the #1 debt snowball calculator and has helped people like us pay off billions of dollars of debt! Just plug in the necessary information about your debt accounts (balance, interest, minimum payment, etc.) and let Undebt.it do the hard work for you.

This program lets you compare total interest, projected payoff dates, and more on the debt avalanche plan and the debt snowball plan. You can even create a custom plan. In a few clicks, see how extra payments will impact your projected payoff date and interest paid.

Using Undebt.it, I found out that I could pay off my debt three months earlier and save $8,430 in interest using the Debt Avalanche method, compared to the Debt Snowball method. However, after an honest talk with myself (yes, you should have this talk with yourself), I accepted the fact that eliminating smaller debts first would keep me engaged, and ultimately will lead to my success!

With the Debt Avalanche method, I would reach my largest debt by the end of 2018, and would only have an extra $155 to put towards it (accumulating prior minimum payments). Using the Debt Snowball method, I will have an extra $1,216 to put towards it. That will be many years from now, but I’m already excited just thinking about it!

Personal finance is (*drumroll please*) personal.

Don’t worry about which method works for your friend or your parents. The most important thing is that you don’t give up. You know which plan will keep you engaged! Maybe saving thousands of dollars in interest is motivating enough for you to stick to the Debt Avalanche method. Or perhaps you’re just starting out on this journey and need a few early victories to get the momentum going.

Just be honest with yourself, and you will be successful!

Are you using one of these debt payoff plans? What are the most significant challenges you’ve faced in your journey to become debt free?